Primer on Bitcoin, NFTs and the ‘Blockchain Revolution’

Over 14 years ago in 2008, an anonymous computer programmer(s) writing under the presumed alias of “Satoshi Nakamoto” developed a groundbreaking new form of digitized currency known as “Bitcoin.” This new currency uses electronic cryptography to generate random numbers, which represent the currency in digital form. As outlined in Nakamato’s ‘White Paper‘ (Bitcoin guide), this new currency was explicitly created as a way to bypass the traditional banking system by allowing “payments to be sent directly from one party to another without going through a financial institution.”

To verify and protect Bitcoin transactions, Nakamoto also created the “blockchain,” a type of digital ledger which serves to securely record transactions using electronic cryptography. The advent of the blockchain also facilitated the invention of the “Non Fungible Token” (NFT), a type of digitized financial security which can be openly traded or sold over the web.

The rise and spread of blockchain technology ushered in a new modern-day gold rush, often referred to as the “Crypto Craze.” While independent artists, investors and billion-dollar currency trading firms have made billions off of this new gold rush, many others have sustained incalculable losses due to the unpredictable and highly volatile nature of the markets. Sometimes these markets collapse—Mt. Gox famously imploded in February 2014—taking many notional fortunes with it.

Cryptocurrency supporters often argue that it is a much-needed new technology with the potential to revolutionize the way money is controlled and distributed, while a growing number of critics are voicing their skepticism and outright opposition to what they see as nothing more than an elaborate, legal scam.

For more on blockchain technology, see our 2018 report: “Blockchain: Revolution or Business as Usual?”

The Origin and Rise of Bitcoin

As the prevalence of blockchain technology grows, so too do the voices of its critics, many of whom include various technological and financial experts, environmental activists, as well as law enforcement officials. Law enforcement, in particular, have always been concerned about cryptocurrency’s ability to obfuscate the identity of its users, which can make it a useful tool for international criminals and political dissidents alike.

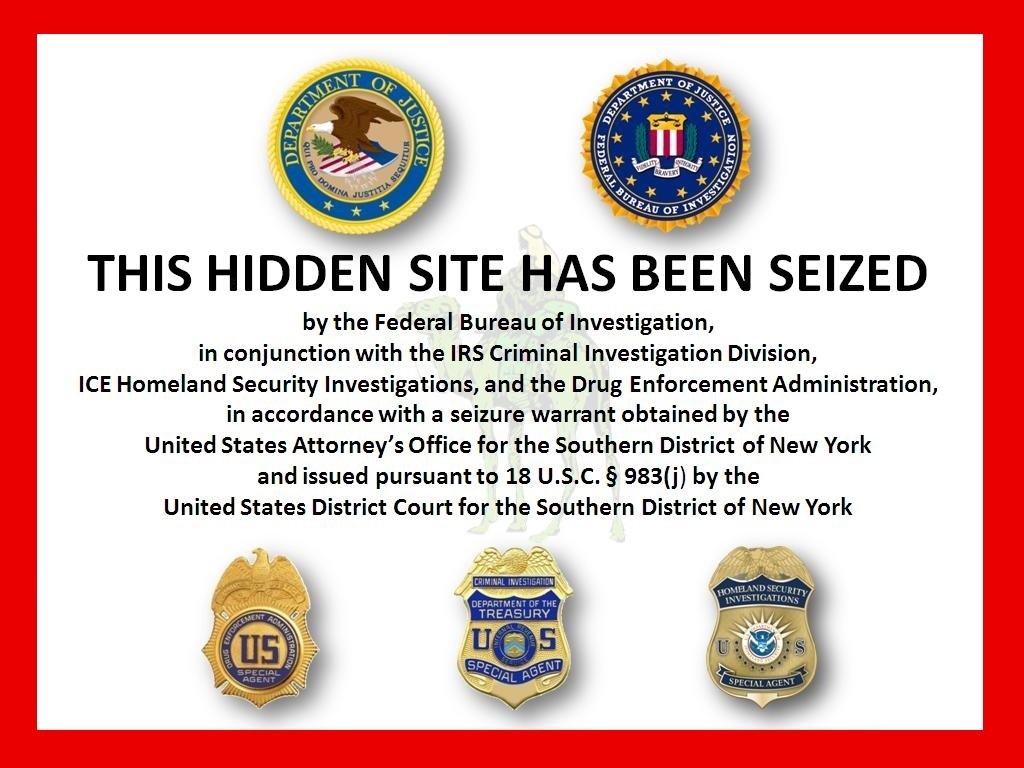

Indeed, cryptocurrency got a major lift in its profile when it became the means of exchange for the illicit underground “Silk Road” website, an online black marketplace where practically anything and everything could be sold in the relative privacy of the “Dark Web.” As the Silk Road grew, it began attracting the attention of federal law enforcement, who subsequently seized the website and arrested its founder Ross Ulbricht in 2013. A series of copycat websites sprang up to take Silk Road’s place, only to be seized and shut down again between 2013 and 2014. The U.S. government claims that since 2020, it has seized at least $1BN dollars in crypto assets connected to the site.

Despite numerous government attempts to regulate, or even in some cases outright ban cryptocurrency, it continues to grow in usage by various criminal organizations, individuals and governments around the world engaging in various crimes, ranging from theft and ransomware payments, to money laundering and even evasion of international sanctions.

While this underground activity is continually growing and evolving, others are even more concerned with the proliferation of above-ground white collar crimes, like market manipulation and fraud.

Learn more about ICE’s Homeland Security Investigations agency in our #Icebreaker series

Ponzi Schemes, Market Manipulation and Fraud

Once ridiculed and shunned by the mainstream financial world, the sharp rise of cryptocurrency millionaires and billionaires in the now estimated $1 trillion dollar market has caused many of those same institutions to reverse course. The subsequent rise of the speculative crypto bubble has seen Bitcoin’s value go from a mere $0.30 per Bitcoin in 2011, to an all-time high of around $66,000 in 2021.

It hasn’t all been roses and butterflies, however, as throughout this period Bitcoin has experienced many radical highs and lows. Most recently, back in June 2022, the market dropped firmly into the sub-$25,000 range, triggered by the billion-dollar cryptocurrency lending company Celsius Network filing for bankruptcy.

Celsius Network LLC essentially operated as a speculative investment bank, holding on to customer’s cryptocurrency assets and lending said assets to prospective borrowers at high interest rates. The bank then assured the lenders that it would recoup their money by paying out high interest rates at later dates. In the mainstream financial world, these investors are comparable to “currency speculators,” or people who buy low-value currencies in the hopes of selling them later at a higher value.

Responding to the worsening cryptocurrency crash on June 13, 2022, Celsius Network CEO Alex Mashinsky put a pause on all withdrawals, but only after withdrawing around $10 million for himself within the same month. Shortly after the company blocked withdrawals, not only did federal authorities begin subpoenaing them for their financial information, but Bitcoin’s overall value fell sharply by another 12 percent.

A month later on July 7, a former Celsius Network lender filed a lawsuit accusing the company of engaging in fraud and market manipulation primarily for Mashinsky’s benefit. The lawsuit is seeking hundreds of millions of dollars in related damages. Six days later on July 13, the company appeared to call it quits, filing for bankruptcy.

To date, the company continues to grapple with multiple civil suits and government investigations which could assist in, but have yet to result in, any criminal prosecution. Despite this, it appears that Mashinsky and the Celsius Network are attempting a rebrand by making yet another cryptocurrency lending company called “Kelvin.”

Observers linked the meteoric growth of crypto market caps, as well as Celsius Network, to the rapid expansion of “stablecoins” which purport to retain a value coupled to the U.S. Dollar on exchanges. While the factors involved are convoluted and shrouded in secrecy, one of the most important stablecoins known as “Tether” was found to have traded without full “backing” during an investigation by the New York Attorney General’s Office that scrutinized the 2017-2018 period. In 2021, business media like Bloomberg and CNBC focused on “Tether’s Billions,” while tech outlets like The Verge tried to address how stable the cryptocurrency actually was. Longtime detractors like “Bitfinex’ed” also probed for intricate details and missing reserve audits.

Cryptocurrency and blockchain technology were promoted as a natural deterrent against wealth concentration, but currently the top 0.01% of Bitcoin holders own more than a quarter of the world’s Bitcoin—a massive wealth imbalance which is even bigger than the top 1% of people who own the lion’s share of the U.S. Dollar. The Celsius Network is just one example of how this wealth imbalance has been used to leverage massive profits, mostly at the expense of its own investors.

Negative Environmental Impacts

In addition to concerns about legal and illegal profiteering, another major criticism revolves around the detrimental impact of blockchain technology on the environment. While exact estimates are hard to come by, a rough estimate from Cambridge University states that the amount of carbon dioxide (CO2) emissions from Bitcoin mining alone could be equal to the carbon footprint of a mid-sized country like Ukraine or Egypt.

The process of creating or “mining” cryptocurrency also contributes to the ever-growing problem of electronic waste, much of which is dumped in poorer, developing nations, leaving those communities exposed to a wide-range of carcinogens and toxic materials.

Producing cryptocurrency creates a large amount of waste because it requires an exceptionally high amount of electricity and computing power, most commonly generated with “application-specific integrated circuit” (ASIC) computer chips. These single-use machines wear out much quicker than the average computer and on average last about a year and a half before they must be discarded and replaced.

As a result, some cryptocurrency advocates have instead opted to support more “environmentally-conscious” alternatives to Bitcoin such as “greencoin,” a cryptocurrency which relies more on solar power to generate the massive amounts of required electricity.

A different cryptocurrency, Ethereum, vastly reduced its energy consumption in September by shifting from “proof of work” to “proof of stake” algorithms, although industry sites report miners simply shifted their rigs into mining other coins regardless.

Growing Popularity of NFTs

As controversial as cryptocurrency has become in recent years, a growing number of critical voices, including some within the cryptocurrency world, have argued that NFTs are much worse.

NFTs first entered the scene shortly after the introduction of Bitcoin in 2013, as a method of trading “uniquely identifiable” digital assets. The first NFT was created by Kevin McCoy with help from Anil Dash on the Namecoin blockchain.

Like cryptocurrency, NFTs are registered and retained in private ‘wallets’ using blockchain algorithms and can be openly traded/sold on the digital market. The main difference is that NFTs are “original works” that theoretically can’t be reproduced—the same signature cannot be sold twice.

However, the ease in which NFT images and videos can be copied and redistributed by simply right-clicking the asset has invoked ridicule and doubts about the supposed security benefits of using the blockchain to control the distribution of such media. At the innermost level, NFTs are often simply designed as bookmarks to servers hosted by companies like Amazon Web Services; the image or video is often not actually embedded within the blockchain itself, since a URL is a far smaller data item to encode.

Even NFT images not publicly accessible over the web are still vulnerable to theft, as was the case with the recent high-profile theft and recovery of actor Seth Green’s “Bored Ape #8398.”

Green originally bought the NFT image for $200,000, naming it “Fred Simian,” intending to use it as a character for his new upcoming cartoon series titled “White Horse Tavern.” Green reported Fred Simian was stolen after clicking on a malicious link in an email addressed to him, falling prey to what is commonly known as a “phishing attack.” The theft had far reaching consequences for Green, as he not only lost the NFT, but also its associated intellectual property rights, making the scheduled production of his new show impossible. Green would go on to make a public plea, promising a hefty reward to anyone who could return the NFT. The thieves would go on to sell the NFT to someone under the alias “Mr. Cheese,” or “@DarkWing84” on Twitter.

Mr. Cheese says that he paid the same amount Green had originally bought the image for, unaware that it had been previously stolen. Due to questionable chances of victory in unprecedented legal territory, Green opted to pay Mr. Cheese 165 Ethereum (ETH) valued at the time around $300,000, or $100,000 more than he originally paid for it.

The increasing occurrence of these hacks have led many to question the effectiveness of using energy intensive cryptographic algorithms to produce digital works which can easily be copied and/or stolen afterward. The site “Web 3 is Going Just Great” charts many of these heists, hacks, and collapsed business entities.

Although some advocates point out how NFTs can be used to benefit disenfranchised artists and activist communities alike, and organizations like “Unicorn DAO” (Decentralized Autonomous Organization) are aiming to do just that. (Unicorn Riot is unaffiliated with Unicorn DAO.)

Assembled in March 2021 by world famous ‘Pussy Riot’ founder Nadezhda Tolokonnikova, Unicorn DAO is dedicated to “collecting and incubating non-fungible tokens created by female, non-binary, and LGBTQ+ artists in Web3.” As such, the organization essentially functions as a platform for “women-identified and lgbtq+ people” to sell their NFTs in a market dominated by cis-gendered men.

Unicorn DAO follows on the success of “Ukraine DAO,” a similar organization also founded by Tolokonnikova which has thus far raised millions of dollars for Ukrainian resistance against the ongoing Russian invasion.

🇺🇦 2250 ETH / $6.75M USD CONTRIBUTED TO THE UKRAINIAN FLAG NFT 🇺🇦

— Ukraine DAO – The Cult of the Armed Forces of 🇺🇦 (@Ukraine_DAO) March 2, 2022

Thank you to all who supported our project 🙏

Next steps: POAP for all those who donated to partybid, work with Come Back Alive on safely transferring funds

You may still donate ETH directly to ukrainedao.eth pic.twitter.com/GsQBLzHIVK

Uncertain Future

While it is currently unknown exactly how many different types of cryptocurrency are currently in circulation, some estimates place that number at roughly around 20,000. Being coupled to the relative value of the most liquid one, Bitcoin, means that many of these currencies have already collapsed as a result of the recent crash. Since June 18 to date, Bitcoin’s value has been hovering at around $20,000 per Bitcoin.

Despite the growing criticism, NFT advocates counter that this new method of trading and distributing digital artwork is a permanent reality of the ever-changing digital landscape. Indeed the NFT market remains a sizable one, currently valued at around $16BN dollars. (Although NFT activity plummeted for much of 2022, it appears to be intensifying again.)

While its trajectory is almost impossible to predict, it’s undeniable that blockchain technology has had an immense influence on the global socioeconomic landscape. “The crypto dons of Beirut” have carved out an alternative niche in difficult circumstances far removed from wealthy Western nations, and demand there is “staggering” as proponents offer to teach the Lebanese people “how to become their own bank.” (The U.S. Dollar, “pegged” to Tether, is worth about 40,000 Lebanese pounds on the unofficial market, and rising.)

Even mainstream institutions like the Switzerland-based Bank for International Settlements have focused all year on developing “central bank digital currencies” (CBDCs) to supplant existing international retail and remittance payment systems.

To its supporters, cryptocurrency is an invaluable resource, providing much needed financial opportunities for people from independent artists, to entrepreneurs and even politically persecuted dissidents. To its detractors, it’s nothing more than an elaborate financial scam whose profits go mostly to financial speculators and criminals, while also representing a significant threat to the natural environment.

Whether cryptocurrency has ultimately been beneficial or detrimental to the Earth and its people is still highly contested. Regardless of what may or may not happen for Bitcoin and NFTs, the idea and concept of a digital currency is likely here to stay.

Learn more about alternative economies in our 2017 reports:

- Greece: Alternative Economies & Community Currencies Pt. 1 – Athens Integral Cooperative

- Greece: Alternative Economies & Community Currencies Pt. 2 – Kenya’s Sarafu-Credit

- Greece: Alternative Economies & Community Currencies Pt. 3 – FairCoop

Follow us on X (aka Twitter), Facebook, YouTube, Vimeo, Instagram, Mastodon, Threads, BlueSky and Patreon.

Please consider a tax-deductible donation to help sustain our horizontally-organized, non-profit media organization: